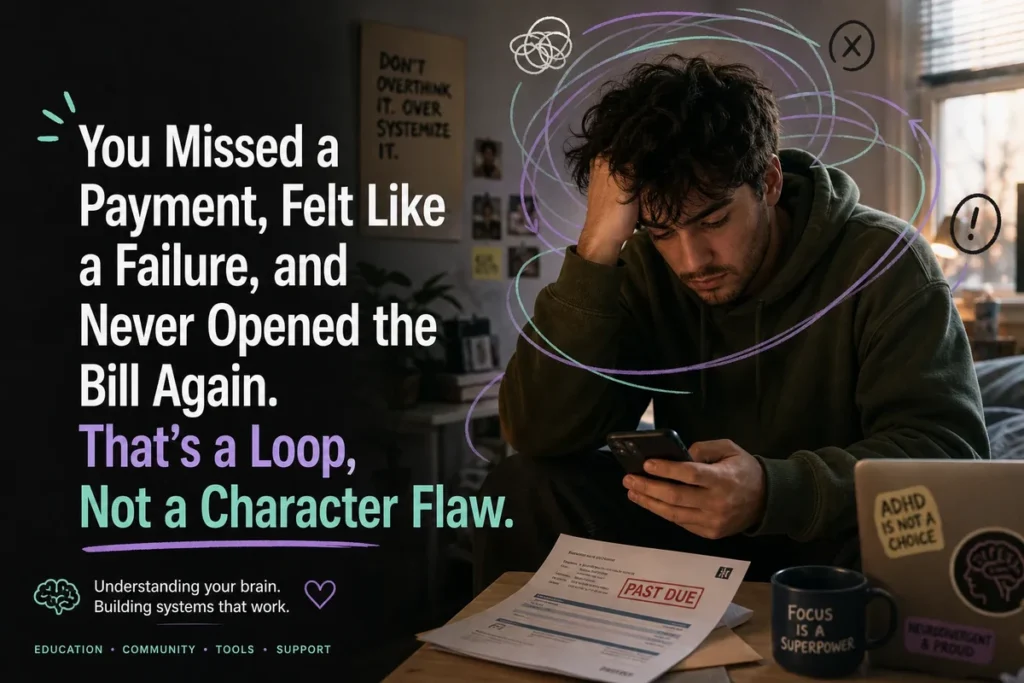

You Missed a Payment, Felt Like a Failure, and Never Opened the Bill Again. That’s a Loop, Not a Character Flaw.

You missed a payment. Not because you didn’t care, not because you were reckless, and not because money genuinely doesn’t matter to you. You missed it because the bill arrived at the wrong moment, your working memory didn’t hold the priority flag long enough, and the due date slipped through a gap that ADHD brains produce dozens of times a year. Then the late fee appeared. Then something happened that had nothing to do with the fee itself: shame arrived, sharp and immediate, and it told you that opening your banking app right now would only make things worse. So you didn’t open it. Then you missed another one. That is not a financial problem wearing a character costume. That is a neurological loop with a predictable three-part structure, and once you can see exactly how it runs, you can start building exits.

Why ADHD Financial Avoidance Is Not What It Looks Like From the Outside

The standard narrative about ADHD and money goes roughly like this: impulsive spending, no budgeting, can’t save, bad with numbers. And while impulsivity is genuinely part of the picture for some people, it misses the more destructive and far less visible pattern: the person who stops engaging with their finances entirely, not because they’re spending recklessly, but because engaging at all has become emotionally unbearable.

This is ADHD financial avoidance, and it operates through shame rather than indifference. The person caught in it often cares intensely about money, thinks about it with anxiety, and knows exactly what they should be doing. The problem is not awareness. The problem is that the act of looking at their account balance has been so thoroughly associated with distress that the nervous system now treats it as a threat to be escaped, not a task to be completed.

Understanding this distinction matters because it changes what intervention looks like. Avoidance driven by shame does not respond to better budgeting apps. It does not respond to being told to “just check your accounts every day.” Those suggestions assume the barrier is logistical. The actual barrier is emotional, and it is running a very efficient neurological program that gets stronger every time avoidance provides even a few minutes of relief.

Phase One: The Miss (And Why It Keeps Happening)

The loop begins with a working memory failure, and this part is worth understanding clearly because most people who live inside the loop blame themselves for something they fundamentally cannot prevent by trying harder.

Working memory, the system that holds information in an active, usable state while you do something else with it, is one of the most consistently impaired functions in ADHD across every developmental stage. Research has shown that working memory deficits in ADHD are not simply about forgetting things. They reflect a failure to maintain information as an active priority once attention shifts elsewhere (Barkley, 2010). A bill arrives. It gets mentally flagged as “deal with this.” Then you answer a text, make dinner, get absorbed in something at work, and the flag quietly drops out of the active queue. It is not laziness. It is a structural property of the ADHD attention system.

Time blindness compounds this significantly. Research on ADHD and time perception consistently shows that many people with ADHD experience the future as neurologically closer to “never” than neurotypical brains tend to do. A due date that is two weeks away does not register as an approaching deadline with appropriate urgency. It registers as vague future time, until suddenly it has already passed. This is not a matter of poor planning intentions. It reflects a genuine difference in how the brain represents future moments as real and imminent.

The miss is not the problem. The miss is a predictable output of a specific neurological architecture. The problem is what happens to the brain in the thirty seconds after the miss arrives as a notification.

Phase Two: The Shame Amplification That Locks the Loop

Emotional dysregulation in ADHD arrives fast and hits hard, and in no domain does it hit harder than in financial failure. When a late fee notification appears on your phone, the ADHD nervous system does not process it as a $25 inconvenience. It processes it through every prior financial fumble, every time someone looked at your account with disappointment, every internal voice that has spent years framing money problems as character evidence.

Research on emotional dysregulation in adults with ADHD estimates that between 30% and 70% experience clinically significant difficulties regulating emotions, with prevalence rates in adults toward the higher end of that range (Shaw, Stringaris, Nigg, and Leibenluft, 2014, American Journal of Psychiatry). That is not a side effect of ADHD. Barkley (2010) has argued that emotional dysregulation should be incorporated into the core theoretical model of ADHD, alongside inattention and hyperactivity, because it mediates so many of the condition’s most impairing outcomes.

The shame produced by financial misses in ADHD is also entangled with something deeper than a single missed payment. Research on ADHD and identity distress has found that adults with the condition, particularly those who reach adulthood without a diagnosis, carry a cumulative burden of perceived failure that attaches to entire domains of life. Money is one of those domains. By the time a person is in their 20s or 30s with undiagnosed or undertreated ADHD, “I am bad with money” has often become a fixed identity claim rather than a description of specific behaviors. The shame is therefore not about today’s missed payment. It is about the verdict that missed payment seems to confirm.

This is the mechanism that turns a single miss into avoidance. The shame is genuinely painful at a neurological level, and the brain responds to pain by doing what it has learned to do: escape.

Phase Three: The Avoidance That Feels Like Relief and Acts Like Poison

Closing the banking app makes you feel better. This is not a character flaw. This is negative reinforcement working exactly as it is designed to work, and the ADHD brain is particularly susceptible to it.

The delay aversion model of ADHD, developed by Sonuga-Barke and colleagues, proposes that people with ADHD have a deficit in signaling for future rewards and therefore develop a learned preference for escaping situations associated with negative affect. Crucially, Sonuga-Barke et al. (2008) found that escape from or avoidance of situations associated with delay-related negative affect is reinforced precisely because it regulates the unpleasant emotional state. The relief is real. And real relief teaches the brain to avoid next time too.

Each time you close the app and the anxiety drops, the neural pathway connecting “financial checking” with “escape response” gets a little stronger. Over weeks and months, the thought of looking at your accounts can begin to generate the avoidance response before you even consciously decide to avoid. This is not weakness. This is conditioning, and it runs on the same mechanisms that drive any avoidance behavior: it works in the short term, which is enough for the brain to keep running it.

The cruel architecture of the loop is that the avoidance which temporarily regulates the shame is precisely the behavior that generates more shame-producing events. More missed payments. More fees. A lower account balance than you realized. More evidence for the verdict the shame was already delivering. The loop tightens itself.

From the community: “I have so much mail I never open. Absolutely not interested in any mail that comes to me. ‘I’ll open it tomorrow,’ I always say. The problem is that tomorrow never comes because it’s always today. It’s gotten me in trouble a few times.”, r/ADHD thread

Why Standard Financial Advice Makes This Worse, Not Better

Standard personal finance advice assumes that the barrier to financial health is informational or habitual: you don’t know how to budget, or you haven’t built the habit yet. The solution is therefore education and routine-building. Track your spending. Make a monthly review date. Know where your money goes.

For someone in an ADHD financial avoidance loop, this advice is not just useless. It actively adds to the shame load. Every article about building a budget, every friend who seems to have their finances effortlessly in order, every financial advice podcast that assumes the listener is engaging with their money rather than hiding from it: all of it becomes more evidence for the verdict. “I know what I’m supposed to do. I still can’t do it. The problem must be me.”

The research on ADHD and decision-making under conditions of negative affect is relevant here. Neuroeconomic studies have found that individuals with ADHD tend toward suboptimal decision-making across varying complexity levels, and that this pattern is partly explained by altered activity in the prefrontal cortex and anterior cingulate cortex (Chachar and Shaikh, 2024, Frontiers in Neuroscience). These are the same regions responsible for processing emotional context in financial decisions. When the emotional content of a financial task is high enough, executive function degrades further, meaning shame does not just hurt. It actively reduces the cognitive capacity available to deal with the thing that produced the shame.

The shame-cognition trap: Research on ADHD and emotional dysregulation shows that negative affect doesn’t just feel bad, it directly degrades the prefrontal executive function you would need to deal with the problem. Shame makes the ADHD brain less capable of the very task it’s shaming you about.

The Wall of Awful in Your Bank Account

ADHD educator Brendan Mahan’s “Wall of Awful” concept describes the invisible emotional barrier that accumulates in front of tasks across a history of associated failure and criticism. Most people think of it in the context of starting a work project or replying to a difficult email. But the Wall is just as present, and often considerably taller, in front of financial tasks.

Every previous missed payment. Every awkward conversation about a bounced check. Every time you transferred money between accounts to cover something and hoped nothing cleared at the wrong moment. Every time someone made a face when they saw your account balance. Every time you promised yourself you’d sort this out and then didn’t. All of that compresses into an emotional obstacle that has to be climbed before any actual financial action can begin. The Wall is why you can spend three weeks thinking about opening your bank account and still not do it. The thinking-about-it time is not procrastination in the casual sense. It is your nervous system preparing to scale something enormous and deciding, repeatedly, that now is not the moment.

This is also why financial shame in ADHD is often invisible to the people closest to you. From the outside it looks like avoidance, or denial, or not caring. From the inside it feels like being unable to move. The gap between those two descriptions is where most of the relationship damage from ADHD financial struggles actually lives. A partner who sees unpaid bills as lack of effort is watching the same behavior through a completely different interpretive frame, and neither person has the language to bridge it without understanding the Wall.

The Wall of Awful in front of financial tasks is not built from indifference. It is built from the accumulated weight of every time this domain confirmed your worst fears about yourself. Tearing it down is not a matter of willpower. It is a matter of reducing the emotional charge one small exposure at a time.

Does Having a Name for This Actually Change Anything?

Understanding that this is a neurological loop rather than a character flaw matters for more than emotional comfort. Shame, particularly the kind of chronic, identity-level shame associated with ADHD financial struggles, has measurable effects on behavior. Research on schema therapy approaches to adult ADHD has identified “defectiveness and shame” as a core maladaptive schema in adults whose ADHD went unrecognized for years: the deep, organizing belief that one is fundamentally flawed and will fail in virtually all endeavors (Shapiro, ADDitude Magazine). When financial avoidance feeds that schema, it is not just creating practical problems. It is reinforcing a story about who you are that reaches far beyond your bank account.

Reframing the loop as a neurological mechanism rather than moral evidence does not make the missed payments disappear. But it changes the emotional information that gets attached to them. A missed payment interpreted as “I am irresponsible and broken” generates more shame and more avoidance. A missed payment interpreted as “my working memory dropped the flag and my nervous system predicted that looking would hurt more than not looking” generates something closer to a problem-solving orientation. The brain can do more with the second interpretation because it points toward interventions rather than verdicts.

For people who arrived at this understanding through late discovery, this reframe often triggers its own grief process. If financial chaos has been running for a decade under the assumption that it was a personal failing, understanding the actual mechanism can feel simultaneously relieving and enraging. Both responses are valid. Understanding the loop does not undo the years of ADHD tax it has already extracted, in fees, in damaged credit, in relationship strain, in the enormous energy cost of carrying shame. It does change what happens next.

What Actually Interrupts the Loop

Breaking ADHD financial avoidance requires working on all three phases of the loop, not just the behavioral output of missing payments. Addressing only the behavior without addressing the shame means the avoidance reflex stays intact and reasserts itself whenever stress rises.

Reducing the cognitive load of the trigger. Working memory failures are not solved by reminders alone, because reminders require working memory to follow up on them. The most effective intervention for bill payment in ADHD is structural elimination: autopay removes the task from the domain of working memory entirely. It is not a workaround or a crutch. It is an accommodation for a specific executive function deficit. Research on ADHD interventions consistently shows that externalized structures outperform internalized strategies, particularly under conditions of stress or emotional load. Set one thing to autopay. Then another. Over time, the financial ecosystem should require as little active working memory participation as possible.

Lowering the emotional temperature of financial contact. Exposure to the financial domain needs to be decoupled from the requirement to fix everything immediately. One practical approach is the “money minute”: a once-weekly, time-limited look at accounts with no action required. The goal is not to budget or plan or solve. The goal is to establish that looking is survivable. This is a direct application of graduated exposure logic, the same mechanism used in treatment for anxiety where avoidance has been reinforced by relief. The nervous system needs evidence that engagement does not inevitably lead to overwhelm before it will stop generating avoidance.

Naming the shame explicitly when it arrives. Research on affect labeling, the practice of naming emotions in specific language, consistently shows it reduces the intensity of the emotional response in the prefrontal cortex. When shame arrives after a financial miss, saying or writing “this is shame, not evidence of my character” is not a platitude. It is a brief but genuinely effective neurological intervention that gives the prefrontal cortex something to work with rather than being overwhelmed by the raw emotional signal.

The structural principle: ADHD-friendly financial systems are not built on discipline or better habits. They are built on removing working memory from the equation wherever possible. Autopay, a balance widget on your phone’s home screen, and a single consolidated account for bills all reduce the number of times your executive function has to show up on time.

The Loop in Relationships

ADHD financial avoidance rarely stays a private problem for long. When it operates inside a relationship, the loop often acquires a second person: a partner who starts managing the bills, who begins to carry the anxiety that the ADHD person cannot access, and who eventually resents both the responsibility and the fact that pointing out the problem produces not engagement but withdrawal.

Clinical reporting on ADHD couples dynamics has found that financial avoidance frequently follows a particular pattern: the non-ADHD partner attempts to introduce accountability, the ADHD partner responds to that attempt as criticism (which it often is, even when well-intentioned), rejection sensitive dysphoria fires, the ADHD partner withdraws or becomes defensive, and the non-ADHD partner doubles down on control as the only alternative to financial chaos. Both people feel alone in it. Neither person is the villain.

Understanding that the avoidance is shame-driven rather than indifference-driven does not dissolve this dynamic automatically. But it provides a different starting point for the conversation. “I know you don’t engage with this because you don’t care” produces a defensive response. “I know you don’t engage with this because looking at it is painful and you’ve learned that not looking makes it hurt less” produces a different one. The ADHD relationships pillar covers this dynamic in more depth, particularly around how rejection sensitive dysphoria and communication patterns intersect in financial disagreements.

Financial avoidance in ADHD is not a relationship failure. It is a pattern that a relationship can accidentally make worse by applying the wrong kind of pressure, or consciously make easier by reducing the shame and changing the structure.

Start Today: Three Actions to Interrupt the Loop Right Now

- Set one bill to autopay today. Pick the recurring bill that causes the most dread, electric, water, rent, phone, and go to that company’s website right now. Set it to autopay from your checking account. This single action removes one working memory task from your system permanently.

- Add your bank balance as a widget to your phone’s home screen within the next hour. Open your banking app, find the widget settings, and place a balance widget on your main home screen where you’ll see it without opening the app. The goal is visibility without friction. Check it once today without judgment or action required.

- When shame about finances arrives this week, name it aloud. The moment you notice financial shame, after a notification, when thinking about bills, whenever the feeling surfaces, say or write: “This is shame about money, not evidence that I am broken.” This small neurological intervention gives your prefrontal cortex something concrete to process beyond the raw emotional signal.

Building Your Way Out, One Structural Change at a Time

The goal is not to become someone who is effortlessly organized about money. The goal is to build a system that doesn’t require your executive function to work perfectly under emotional stress in order to avoid a late fee. Those are very different targets, and only one of them is achievable.

Start with autopay for every recurring bill you can automate. Not as a resolution or a vow, but as a structural change that removes a category of working memory demand entirely. Then look at account visibility: a banking app widget on your phone’s home screen that shows your balance without requiring you to open anything means financial reality stays in your peripheral awareness rather than behind a barrier you have to summon motivation to open. Small, low-friction visibility changes reduce the startle response when you do eventually engage.

The ADHD money pillar has a fuller breakdown of financial systems built specifically for ADHD brains, including tools for dealing with the ADHD tax that missed payments and late fees represent. The key principle running through all of it is consistent: every element of financial management that requires you to remember, initiate, or tolerate emotional discomfort on a recurring basis is a liability. Every element that happens automatically, is visible without effort, and doesn’t require you to feel capable before it activates is an asset.

None of this is about becoming “good with money.” It is about designing around the actual architecture of your brain, rather than continuing to try to run a system built for a different one. The loop is not a character flaw. It has never been a character flaw. It is a predictable output of a nervous system that learned to escape pain, trying to function in a financial world that assumes everyone’s working memory is intact and that shame is motivating rather than paralyzing. Changing the architecture changes the output. That part is genuinely possible.

Rate this article

Was this a useful hit?