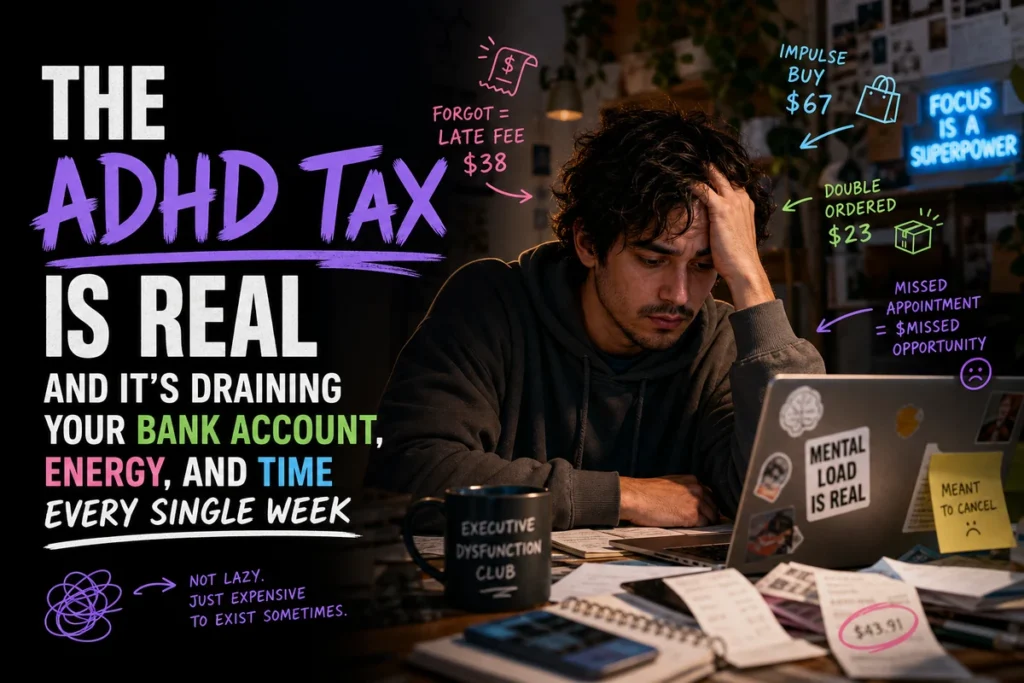

The ADHD Tax Is Real and It’s Draining Your Bank Account, Energy, and Time Every Single Week

The ADHD tax is not a metaphor. It is the measurable, compounding financial and energetic cost of living in a world designed for brains that naturally do the things yours requires enormous effort to do: remember recurring obligations, resist the pull of immediate reward, return phone calls, read the fine print, and act on the boring thing before it becomes an expensive emergency. If you have ADHD and you have wondered why you feel perpetually behind financially despite earning a reasonable income, this is where to start looking. Not at your spending habits as a character flaw, but at the structural friction your neurology creates at every point where money and time intersect.

What the ADHD Tax Actually Costs: The Numbers Have a Shape

Most conversations about ADHD and money stop at “impulsive spending.” That framing, while not wrong, dramatically understates the problem. The ADHD tax is not a single line item. It is a recurring, multi-category drain that compounds across your entire adult life. It includes the obvious: late fees, overdraft charges, missed insurance deadlines, lapsed subscriptions you forgot to cancel. But it also includes the invisible: the premium you pay on convenience purchases because you left the house without food and are now buying an overpriced sandwich, the duplicate charger you bought because the original is in a bag you cannot locate, the parking ticket because time blindness made you 40 minutes late and you didn’t read the sign properly, the therapy session you paid for and forgot to attend.

Research by Deloitte Access Economics, commissioned in 2019, estimated the total social and economic cost of ADHD in Australia at over AUD 20 billion annually. That figure includes direct costs like healthcare and treatment, but also the productivity losses, educational underachievement, and employment instability that stem from unmanaged ADHD. The per-person economic impact is substantial, and the research makes clear that the costs are not primarily driven by “bad decisions” in the abstract. They are driven by specific, well-documented neurological mechanisms that operate below the level of conscious choice.

The ADHD tax is not a single bad decision. It is thousands of small decisions that your neurological architecture consistently nudges in the costlier direction, across decades.

Chachar and Shaikh (2024, Frontiers in Neuroscience) synthesized the neuroeconomic research and found that individuals with ADHD tend toward suboptimal decision-making across economic contexts, choosing options with lower expected value even when better alternatives are visible. This is not about risk appetite alone. It is about how the prefrontal cortex, striatum, and anterior cingulate cortex process options, evaluate feedback, and generate inhibitory control. When these systems are running with reduced efficiency, every financial decision point becomes harder, slower, and more likely to produce a suboptimal outcome.

Why the “Just Make a Budget” Advice Fails So Completely

Standard financial advice assumes a specific cognitive architecture: the ability to hold future costs in mind with sufficient emotional weight to override present-moment impulses. For a significant portion of the population, this is straightforward. For ADHD brains, it runs headlong into a documented neurobiological reality called delay discounting.

Ikegami et al. (2026, BMC Psychology) used structural equation modeling to map the precise pathway by which ADHD traits produce poor decision-making. Their findings identified a sequential cascade: steeper delay discounting (preferring smaller immediate rewards over larger future ones) leads to reduced sustained attention, which compounds with working memory errors, and together these produce suboptimal decision-making directly associated with elevated ADHD traits. The key takeaway is that the problem is not one thing. It is a chain reaction. And budgeting advice, which operates entirely at the conscious-planning level, intervenes nowhere along that chain.

This is also why “just think about your long-term goals” is such useless advice for ADHD adults managing money. Future-oriented goal representations generate less motivational signal in hypodopaminergic fronto-striatal systems. The emergency fund you need in six months is neurologically quieter at the moment of decision than the item on the screen in front of you right now. This is not a values failure. It is a hardware specification.

What “suboptimal decision-making” really means: Neuroeconomic research distinguishes ADHD financial behaviour as suboptimal rather than merely risky. People with ADHD do not just choose high-stakes gambles, they consistently select lower-value options across contexts. The problem is not boldness. It is that the brain’s evaluation machinery for future outcomes is structurally underweighted relative to present-moment pull (Chachar &, Shaikh, 2024, Frontiers in Neuroscience).

The Six Channels Where the ADHD Tax Flows

To reduce the ADHD tax, you need to name every channel it flows through. Most people with ADHD are aware of one or two. The full list is usually much longer, and the compound effect is what makes it financially significant.

Late fees and penalty charges. Bills get forgotten not because you don’t care, but because the working memory system that should be flagging “this is due in three days” fails to keep it active once it leaves your immediate environment. Grinblat and Rosenblum (2025, Brain Sciences) demonstrated that adults with ADHD showed significantly poorer organization-in-time compared to controls, and that this temporal disorganization was directly associated with reduced quality of life across health, work, and financial domains. Every time a bill drops out of your active mental field, you are one step closer to a fee.

Duplicate purchases. You buy scissors. You cannot find the scissors. You buy another pair. You later find three pairs of scissors in various bags and drawers. ADHD object permanence, the working memory failure that makes things functionally cease to exist when they leave your field of view, drives a category of spending that is almost invisible in standard budget analyses but accumulates rapidly. The item is not wasted money in any single transaction. The pattern is the problem.

Impulse and panic purchases. Two distinct mechanisms generate this cost. The first is true impulsivity: the dopaminergic pull toward immediate reward before the prefrontal brake can engage. The second, less discussed, is panic purchasing: buying the overpriced item, the rushed service, the last-minute delivery, because the ADHD brain chronically underestimates how long things take and runs out of time to plan. Both pathways arrive at the same destination, spending more than you intended in a moment of low executive function availability.

Lapsed subscriptions and memberships. Signing up requires novelty-driven dopamine. Cancelling requires noticing that something has become irrelevant, then scheduling and executing the cancellation. For ADHD brains, the first half of that equation is easy. The second half requires exactly the kind of low-urgency, future-oriented self-monitoring that working memory deficits make unreliable. Subscriptions to services last used in a previous era of your life continue billing because the brain’s reminder system, the one that should surface “you haven’t used this in four months,” does not fire reliably.

Missed appointments and no-show fees. This one layers time blindness on top of working memory failure. You knew about the appointment. You intended to go. But the ADHD brain’s relationship with prospective memory, the ability to execute a future intention at the right moment, is often significantly impaired. Barkley (1997, Psychological Bulletin) established behavioral inhibition and working memory deficits as central to ADHD, not peripheral to it, and prospective memory failures are a direct downstream consequence. The missed GP appointment, the rescheduling fee, the specialist cancellation charge: these are not carelessness. They are predictable outputs of a specific cognitive deficit.

Decision fatigue and the cost of inaction. ADHD brains carry an unusually high cognitive load. Every task that requires switching, planning, or self-monitoring costs more executive function than it would for a neurotypical brain. By mid-afternoon on many days, the decision-making capacity that was available in the morning is largely depleted. This is when the expensive food delivery order happens instead of cooking. This is when the insurance comparison gets deferred for another month. This is when the “I’ll deal with it later” that becomes a late fee is born. The inaction itself carries a price.

From the community: “I was supposed to have a phone call today, and I put it off for over three hours. I really dislike phone calls and prefer texting, but most people are the opposite.”, r/ADHDmemes thread

That phone avoidance is not trivial. Every unmade call involving a billing dispute, a prescription renewal, a service cancellation, or a benefit claim is a potential ADHD tax waiting to be charged. The friction of phone-based tasks is a real and specific barrier that money management systems built for neurotypical people almost completely ignore.

The Energy Cost Nobody Puts a Number On

The financial ADHD tax has a twin: the energetic ADHD tax. And the two are deeply intertwined. Research consistently shows that adults with ADHD report lower quality of life across multiple domains, and that the predictors of this lower quality of life are not the ADHD traits themselves so much as the executive function deficits and temporal disorganization those traits drive (Grinblat &, Rosenblum, 2025, Brain Sciences). Every financial near-miss that gets narrowly avoided, every late fee you catch in time, every panic cancellation you scramble through, costs cognitive bandwidth. That bandwidth is finite.

The result is what clinicians sometimes call the ADHD effort tax: the additional mental overhead required to operate in a world not designed for your brain. Compensatory strategies, keeping a dozen tabs open so you don’t forget things, setting seventeen alarms, rechecking the same information multiple times because you don’t trust your memory, are exhausting. They work sometimes, but they burn fuel that a neurotypical person doesn’t have to spend to achieve the same outcome. This is part of why ADHD burnout is so common, and why financial stress and overall exhaustion often arrive together. They share the same underlying cause.

Compensating for ADHD friction with raw effort is not a long-term strategy. It is a high-cost workaround that delays burnout without preventing it.

Why This Is a Systems Problem, Not a Discipline Problem

The ADHD tax is sometimes framed as a tax on impulsivity, which implies that more self-control would reduce it. This framing is both inaccurate and counterproductive. The actual tax is a tax on system design, specifically on the absence of systems engineered for the cognitive profile of ADHD. A neurotypical person operating without systems still does reasonably well, because their default cognitive architecture handles many of the background tasks automatically: the prospective memory, the delayed gratification, the cost-benefit calculation across time. An ADHD brain operating without systems is at the mercy of exactly the mechanisms that produce suboptimal outcomes.

The corrective intervention is environmental design, not willpower. This is not a feel-good reframe. It is the practical implication of the neuroeconomic research. If the problem is that future costs are neurologically quieter than present rewards, the solution is to make the future cost loud and present, not to try harder to hear it. If the problem is that bills leave working memory when they leave the field of view, the solution is to remove working memory from the loop entirely, not to try to remember harder.

This connects directly to what the ADHD Systems pillar is built around: the architecture of your environment matters more than the intensity of your intention. And for ADHD money management specifically, this means designing friction into spending and designing friction out of paying.

What Environmental Design Actually Looks Like for the ADHD Tax

The following is not a list of generic tips. It is a framework of structural interventions, each targeting a specific neurological mechanism that produces ADHD tax.

Automate all recurring obligations. Autopay is not laziness. It is the correct response to a working memory system that cannot reliably maintain low-salience recurring obligations. Rent, utilities, minimum credit card payments, subscriptions you actually use: every one of these that remains on manual payment is a point where the ADHD tax can be charged. The setup cost is one hour. The protection lasts indefinitely. This is the single highest-leverage intervention for ADHD late fees.

Design a visible financial system. ADHD object permanence means that financial obligations living in folders, email inboxes, or apps you check irregularly functionally cease to exist between check-ins. The solution is to make the financial picture visible, not occasionally but as a permanent feature of your environment. A whiteboard with three numbers (amount owed, due date, balance) on a wall you pass every day will outperform any budgeting app that requires you to open it. Visibility is the intervention. The tool is secondary.

Add friction to impulsive spending. Because your brain may not reliably generate internal friction at the moment of a purchase impulse, the friction has to be environmental. A 48-hour rule for any non-essential purchase over a set threshold. A single-use virtual card number for online shopping that requires regeneration each time, slowing the process enough for executive function to engage. Removing saved card details from retail sites. Each of these adds one small step between impulse and action, and that step can be enough to let the prefrontal cortex catch up.

Audit for ghost subscriptions quarterly. Set a recurring calendar block every three months specifically to scan bank and credit card statements for recurring charges. Not because you will remember to cancel things when they become irrelevant, but because you have accepted that you won’t, and you’re building the review mechanism into the schedule instead. This audit often reveals significant monthly leakage that accumulates invisibly.

Reduce the phone-call requirement. Phone avoidance is a genuine barrier for many ADHD adults, and many financial tasks still require calls. Identify which of your recurring financial obligations can be handled via online account management, text, or email instead. Where phone calls are unavoidable, batch them into a single scheduled block during your peak executive function window, typically mid-morning for many ADHD adults, and treat the block like a fixed appointment.

The goal is not to become someone who manages money effortlessly. The goal is to build a system where the most common failure modes cannot generate a charge.

The Time Cost: Where Hours Disappear Into ADHD Friction

The ADHD tax is also a time tax. Every administrative crisis, every emergency trip to replace something lost, every hour spent navigating a billing dispute that a timely payment would have avoided, every morning derailed by the chaos of misplaced keys: these are hours. And for many ADHD adults, they add up to significant weekly time spent in reactive, high-stress, friction-heavy activity rather than anything chosen or productive.

Time blindness amplifies this significantly. The research on time organization in adult ADHD, including the Grinblat and Rosenblum (2025) study, demonstrates that temporal disorganization is not a peripheral trait but a core contributor to impaired daily functioning and reduced quality of life. When your brain often cannot reliably perceive time and cannot maintain a dependable internal schedule, the practical result is chronic underestimation of task duration and a pattern of arriving at every obligation already behind. The cognitive cost of this chronic time deficit is enormous, and it interacts with financial outcomes in direct and measurable ways.

The compound effect: The individual costs of ADHD friction, a single late fee, one panic purchase, one missed appointment, are rarely catastrophic on their own. The ADHD tax becomes a serious financial problem through repetition and accumulation over months and years. A 2019 economic analysis by Deloitte Access Economics estimated the total annual cost of ADHD in Australia at over AUD 20 billion, with individual-level productivity and financial losses representing a major share. The mechanism is compound friction, not single events.

Does Medication Reduce the ADHD Tax?

Research suggests that stimulant medication can meaningfully improve the executive function deficits that drive the ADHD tax, including working memory, response inhibition, and delay discounting. Shiels et al. (2009, Experimental and Clinical Psychopharmacology) found that methylphenidate reduced discounting of delayed rewards in participants with ADHD, suggesting that the neurological bias toward immediate reward is at least partially addressable pharmacologically. For adults, this can translate to more consistent follow-through on financial obligations, less impulsive spending, and improved planning capacity.

But medication is not a complete solution to the ADHD tax, for several reasons. First, it is not effective for all people and all ADHD presentations. Second, even well-medicated ADHD adults often retain some degree of executive function variability, particularly when medication wears off, during periods of stress, or during hormonal fluctuations. Third, medication addresses the neurological substrate but does not automatically install the systems and habits that reduce friction. The most effective approach combines whatever pharmacological support is appropriate with environmental design that does not depend on any given day’s executive function availability.

Reframing: The ADHD Tax Is a Design Failure, Not a Moral One

One of the most damaging things about the ADHD tax is not the money or the time. It is what the pattern of losses does to your self-narrative. Every late fee feels like evidence of irresponsibility. Every duplicate purchase feels like proof of carelessness. Every missed appointment feels like confirmation of a story about who you are. The shame accumulates alongside the financial losses, and it is often the shame that makes the problem harder to solve, because it frames the solution as “become a different person” rather than “design a different environment.”

The neuroeconomic research is useful here precisely because it is precise. The losses are not random. They follow specific, well-understood patterns driven by specific, well-documented mechanisms: delay discounting, working memory deficits, temporal disorganization, impulse regulation. Each of these is addressable, not by trying harder, but by designing around the failure mode. This is the same logic that produces guardrails on mountain roads. You do not fix the road by asking drivers to be more careful. You put the guardrail where the car would otherwise go.

The existing article on ADHD financial planning and reward architecture covers the neurochemistry of why future goals feel less real than immediate spending urges. This piece is the companion: what the compounding friction actually costs, where it comes from, and what a properly designed environment can do to interrupt it. Neither piece is about becoming more disciplined. Both are about understanding the exact shape of the problem well enough to engineer something that works around it rather than demanding that your brain become something it is not.

The ADHD tax is real. It is also, more than most financial problems, a problem with a structural solution. Build the system. Let the system do the remembering. Your brain was never meant to carry this load alone.

Quick Dopamine Hits:

- Set every bill, subscription, and rent payment to auto-pay today. Open your bank app right now and enable autopay for any outstanding accounts, remove the requirement for your brain to remember.

- Buy one duplicate-prevention kit: a second charger, a second set of keys, a spare of the thing you buy in panic most often. The upfront cost is always less than the cumulative ADHD tax you pay replacing it.

- Create a single ‘financial inbox’: one folder or note where every financial decision that isn’t urgent goes to sit for 48 hours before you act on it. This adds friction to impulsive spending and creates a review window your brain can actually use.

Rate this article

Was this a useful hit?